")

")

Darden Restaurants, Inc. (NYSE:DRI) has been able to generate a total shareholder return of over 10% annually on any 10 years since its spin-off from General Mills 29 years ago. As a result, it returned 363% vs. the 176% the S&P500 (SPY) achieved.

However, in the past 5 years, DRI shares’ return has only been 42% versus the S&P500 returning 88%. Even worse, in the past year, we have the index returning over 24% while Darden’s stock is down 8%.

We are in an interesting situation. If we find out Darden can still deliver its 10% TSR over 10 years, we would have a stock in the perfect situation for us to jump in and benefit from the expected ride-up, which, to even things out, should compound at a faster pace than 10% annually.

On the other, we might find some reasons that explain the slowdown of the company, at least from the perspective of its stock performance.

As Darden’s Q4 earnings approach, I want to initiate my coverage of this company, giving my preview of the earnings report and sharing my take and what could be the best strategy to play the stock.

Darden Restaurants: The Company

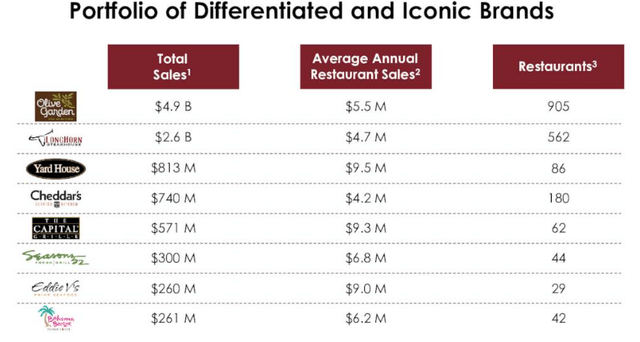

First of all, Darden Restaurants is a full-service restaurant company, owning and running 1,914 restaurants at the end of its last fiscal year. Its brand portfolio sees 8 iconic names, with the addition of a ninth brand – Ruth’s Chris Steak House, whose acquisition was completed on June 14, 2023. As a result, we will see this brand incorporated in the upcoming annual report for the first time. The brands Darden owns and operates are Olive Garden, LongHorn Steakhouse, Cheddar’s Scratch Kitchen, Yard House, The Capital Grille, Seasons 52, Bahama Breeze, and Eddie V’s Prime Seafood. Below, we see the size of each brand.

DRI Q4 2023 Presentation

In FY 2023, Darden grossed $10.49 billion in sales. This means Olive Garden alone makes up 46.7% of total sales while accounting for 47.3% of total restaurants. The little difference between the impact on sales comes from the portfolio mix, with Olive Garden targeting lower-income consumers, while most of the other brands are focused on fine dining and its higher profits.

The second largest brand for Darden is LongHorn Steakhouse, which makes up 24.8% of total sales and has 29.4% of the company’s restaurants.

So, the two largest brands account for over 70% of Darden’s sales, which means the company is fundamentally driven and influenced by the performance of these two brands. As a result, Darden has four reportable segments: Olive Garden, LongHorn Steakhouse, Fine Dining, and Other Business.

As a matter of fact, I have come to research Darden because of LongHorn Steakhouse. In fact, I am personally invested in Texas Roadhouse, Inc. (TXRH), which is one of its main competitors. This is why I will pay closer attention to this brand in this analysis.

Darden Restaurants Financials

Darden’s financials show a well-managed company.

Its top line keeps growing rather steadily and this is key for restaurants (5.3% 10 yr-CAGR). Being low margin businesses, driving top-line growth both through location expansion and comparable sales growth is crucial to reach a large enough scale to become profitable and successful. Its operating income has compounded 13.3% annually for the last ten years, thanks to moderating SG&A and operating expenses. Thanks to some share repurchases, mainly executed in 2022 and 2023, the company’s EPS has compounded even faster at 14% annually. This is a solid base to drive the stock’s appreciation up.

The company’s balance sheet is solid, though its debt is a bit high. In fact, at the end of its last fiscal year, Darden reported $368 million in cash and $1.37 billion in LT debt. Its total equity has been rather stable, hovering around $2.2 for the past ten years (except for the Covid-affected FY 2021 where the company’s retained earnings of $522 million increased to $2.8 billion). This is important because the best metric Darden has is its ROE, which is currently over 49%.

Moving on to DRI’s cash flow statement, we see the company’s FCF compounding 10% per year over the last decade, moving up from $355 million in FY 2024 to $931 million at the end of the last fiscal year. With the acquisition of Ruth’s Chris and the company’s organic growth across its other brands, we should expect it to post $1 billion in FCF soon.

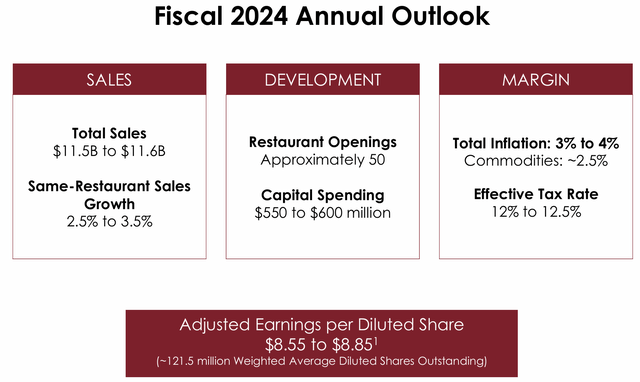

Darden in fiscal 2024

Darden started the year expecting revenues to keep their growth and come above $11.5 billion, driven by expected comp sales growth of around 3% and 50 new restaurant openings.

However, as Darden sailed through its fiscal year, it had to face some unexpected challenges. In particular, its comp sales growth didn’t come in as expected due to lower-income consumers pulling back on casual and fine dining spending.

This is what Darden’s CEO, Mr. Cardenas, explained to the market during the March Q3 earnings call that

We experienced some underlying softness we had not seen in the months leading up to January. The lower-income consumer does appear to be pulling back, and the mix of guests based on income is now in line with pre-COVID. […] Transactions from households with incomes above $150,000 were higher than last year. Transactions from incomes below $75,000 were much lower than last year. And at every brand, transactions fell from incomes below $50,000. Similar to Q2, this shift was most pronounced in our fine dining segment. […] According to Black Box, every segment in the industry, from QSR and up was negative in same-restaurant traffic in our third quarter, every one of them. So that’s also a year-over-year phenomenon. And so we’ll continue to monitor what we see with the guest and what we see on that lower-end consumer.

I think the picture Mr. Cardenas paints is no surprise for most of us. We all know lower-income consumers are feeling inflationary pressure more than others. However, while the industry may have indeed performed worse than in the past, while every segment may be down, some restaurants keep on growing, nonetheless. This is the case with Texas Roadhouse, as we will see in a moment.

This environment, according to Darden, explains the cause of same-restaurant sales decreases by 1%. At the same time, Darden’s management stated that the company outperformed the industry since its comp sales were 320 bps better than the average.

However, thanks to moderating commodities inflation, which Darden reported to be around 1.5% vs. the 3.5% of its guidance at the beginning of the year, the company’s EBITDA margin was 20.6%, 70 bps better than a year ago. Now, for a restaurant company, this is a very good margin.

But we said that Darden’s performance mainly depends on Olive Garden and LongHorn Steakhouse. How have these two performed so far?

In Q3, Olive Garden increased its total sales by 0.7% to $1.31 billion. Considering the company’s restaurant count has grown by 12 units to 917, we can easily infer that Olive Garden’s comparable sales decreased. Olive Garden’s check was up 2% in the quarter, so what dragged down its performance was lower traffic, which was reported to be -3.8%.

The same wasn’t true for LongHorn. Its quarterly sales were $731 million in Q3 and $2.04 billion for the nine months ended in Q3. This is a 5.1% increase YoY for the quarter and +7.3% for the nine months. At the same time, its restaurants increased by 10 units to 572 (+1.8%). This means its same-restaurant sales did actually increase. In fact, during the last earnings call, Darden stated its comp sales growth was 2.3%, which equals to a 650 bps outperformance versus the industry. At the same time, LongHorn’s traffic was down around 2.5%. LongHorn Steakhouse’s profit margin was 18.7% which, again is high for this kind of restaurant.

Interestingly, Dardens’ management explained why LongHorn performed better than Olive Garden:

Steak does a little bit better when beef prices are higher just because of the relative gap between the consumers who would rather not take a risk on cooking something expensive.

LongHorn Steakhouse vs. Texas Roadhouse

This paragraph may hurt someone’s feelings. I often find comparisons over the Internet, with many customers polarizing in one sense or the other, often appearing more as fans, rather than consumers.

In any case, many appreciate LongHorn’s steak display and quieter environment, but others can’t just give up Texas Roadhouse’s fresh rolls with honey cinnamon butter in a rowdier atmosphere. The fight ignites when comparing the cheaper 8-ounce steak at Texas Roadhouse, vs. the more expensive, yet larger 9-ounce steak at LongHorn. With the 20-ounce ribeye, people argue in favor of Texas Roadhouse’s better pricing, versus LongHorn’s higher quality. Texas Roadhouse is a dinner-only concept, so for people craving a steak for lunch, the option is only one.

Here, I want to focus on what the financials say, because I think they shed some light on this competition.

In its February Q4 2024 earnings call, Texas Roadhouse reported comp sales growth of over 10%. It was even more countertrend when it disclosed that more than half of that increase came from higher guest traffic. In an environment like the one we have seen, where, in any case, LongHorn did hold up fairly well without taking too large of a hit, what Texas Roadhouse reported was outstanding.

Its revenue growth for the fiscal year was 15.3%, supported by a 9.3% increase in average unit volume and 6.1% store-week growth. Restaurant margin dollar increased by 21.4% to $177 million, and a diluted EPS increase of 21.3% to $1.08 was reported, too.

In its last quarter of the fiscal year, Texas Roadhouse reported average weekly sales of over $141k per store, 12.6% of which came from to-go orders. Comp sales increased 9.9%, thanks to a 5.1% traffic growth and a 4.8% increase in average check.

I think there is no way around it, Texas Roadhouse is gaining momentum and the consumer’s preference, since the company was among the very few able to report increasing KPIs all across the board.

The trend continued when Texas Roadhouse reported its May Q1 FY24 earnings call, revenue of over $1.3 billion (12.5% growth), and same-store sales growth of 8.4%, driven by a 7.7% increase in average unit volume and a 4.9% store week growth. Checks increased by 4.1%. Restaurant margin dollars increased to $228 million (+23%) and diluted EPS increased a staggering 31.4% to $1.69.

Average weekly sales were $159k (in Q4 we had $141k!)

By month, Texas Roadhouse comp sales grew 4.2%, 10.4%, and 10.2% for the January, and February March periods respectively.

Moreover, Texas Roadhouse disclosed its comp sales for the first five weeks of Q2 were up 9.3% with weekly average sales already up to almost $158k.

Keep in mind that LongHorn would be happy to post flat to positive low single-digit results.

Before these numbers, there is no doubt Texas Roadhouse’s operations are stronger than LongHorn’s.

Given this situation, what should we expect from Darden’s Q4 and FY24 earnings?

Darden Q4 FY 2024 Earnings Preview

Let’s start with the outlook Darden released at the beginning of the fiscal year it has recently ended. We see Darden expecting total sales between $11.5 billion to $11.6 billion, with same-store sales growth between 2.5% to 3.5% and EPS forecasted to be between $8.55 and $8.85.

DRI Q4 FY23 Earnings Presentation

However, at the end of Q3, Darden updated its fiscal 2024 outlook, by lowering its total sales expectation to $11.4 billion and its comparable sales growth to 1.5% to 2.0% instead of the 2.5%-3.5% range. Restaurant openings should be above 50, but no more than 55. Capital spending is confirmed at $600 million. Total inflation has actually come down to 3% with commodities now at 1.5% instead of the 2.5% expected at the beginning of the year. As a result, though Darden’s top line saw some extra weakness, the company’s EPS will come above the prior guidance and should be in the range between $8.80 and $8.90. This means Darden is trading around a 16.5 2024 PE.

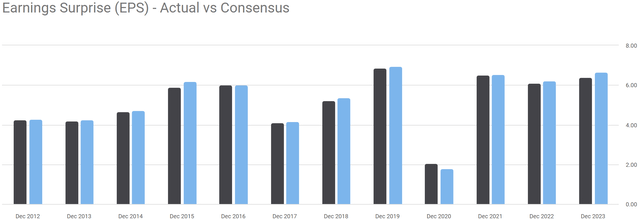

Now, if we look at Darden’s past history, we see that its EPS has given almost no surprise, coming always very close to the consensus estimates.

Seeking Alpha

This is because the company does execute at a constant pace with good efficiency.

Currently, consensus expects Darden to report $11.41 billion in revenue and EPS of $8.84, perfectly in line with the Q3 guidance. I believe analysts have learned that Darden more or less delivers what it guides for.

In this current environment, I don’t think Texas Roadhouse is the right peer to assume the whole environment is turning in favor of Darden’s restaurants. As I have shown, Texas Roadhouse is outperforming because of its particular customer attraction strength and its execution. However, what we learned from Texas Roadhouse may hint that the consumer is not pulling off from discretionary spending more aggressively than in the past. So, there are reasons to believe LongHorn will report revenue growth and flat comp sales.

Overall, Olive Garden may suffer a little more. But the overall picture shows Darden should hold up fairly well and will likely come very close to the consensus estimates.

As a result, Darden’s forward P/E of around 16.5 is quite accurate in my opinion, as well as Darden’s 2025 forward P/E which should be around 15.5, if we consider 8% revenue growth next year.

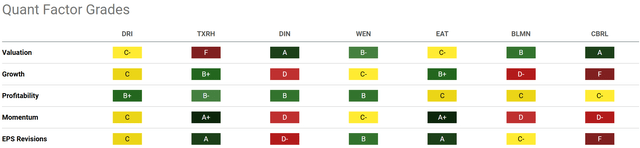

If we compare Darden to several competitors, such as Dine Brands Global, Inc. (DIN), Brinker International, Inc. (EAT), Bloomin’ Brands, Inc. (BLMN), and Cracker Barrel Old Country Store, Inc. (CBRL), we see that, aside from valuation, Texas Roadhouse beats everyone across the board. Darden, however, slightly wins under profitability, earning a B+.

Seeking Alpha

At the same time, Darden’s valuation is graded with a C-, showing there might be some value here. However, Quant Grades are quite clear this time: the C is not mispricing, but it reflects the other Cs we see under growth, momentum, and EPS revisions.

Considering the stock trades at a 16.5 forward P/E and is struggling to report strong comp sales growth, I think we are before a fair valuation. What could we do? To those already invested in Darden, I would not suggest exiting the position, as I see no particular concerns. To those wanting to jump in, it would be advisable to either start dollar cost averaging or wait for this report to see if Darden shows some signs of new strength relative to comp sales growth.

A buy could also be a strategy if we consider Darden able to compound 10% annually over a 10-year horizon. As said at the beginning, if we expect this to happen, Darden would be a very interesting buy right now because of its recent trading history with little stock appreciation.

As for me, I have enough interest in the company to add it to my watchlist, but, being invested in Texas Roadhouse, I still prefer to stick with my holdings without adding Darden right now.

Read the full article here

")

")

")

")

Place In Emerging Quantum Computing Field")

")

")