")

")

Introduction

After a few attempts in the past year or so, I have decided that now is the time for me to go long with the US REIT market, which is due for a recovery in 2024. I am constructing my REIT portfolio as part of the income bucket (with a 6% dividend threshold to make the cut) as well as the total value return bucket (with the beaten down sectors).

One of my favorite choices for REIT holdings is Cohen & Steers REIT & Preferred Income Fund (NYSE:RNP). Cohen & Steers is known for managing some of the best CEFs in this space, RNP is one of the CEF funds with a focus on top-quality REITs. Combined with high-yield bond holdings, it pays 7.89% monthly dividend that makes it attractive and competitive in the current income market. Its ETF counterparts, such as the most popular REIT ETF VNQ, pay dividends about only half of the yield. RNP uses high leverage, with Effective Leverage at 31.53%. With moderate rate cut is expected from FED in the foreseeable future, RNP’s high leverage may start to bring positive outcomes to the fund’s return as it is designed for. I recommend RNP to high-yield seekers who also want to be ready for a sizeable REIT recovery in 2024 and beyond.

RNP Fund Premier

RNP is a closed-end fund that was incepted in June 2003 and managed by Cohen & Steers, one of the best asset managers in the business. The fund’s main objective is to offer high-yield income, and the capital appreciation is the secondary goal. The strategy RNP deploys to accomplish its objectives is to invest in REIT stocks, the preferred shares and other debt securities such as corporate bonds.

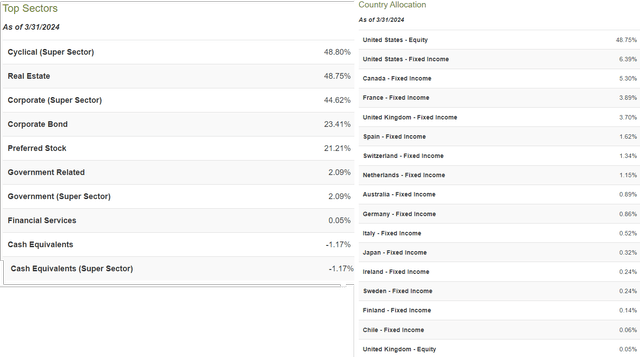

The fund is global in nature and invests in many countries all over the world. It has over 48% of investments in the US equity market, with Canada and France coming in the distant second and third place. Other countries invested are the U.K., Spain, Switzerland, Netherlands, and a few others with very small weights.

The following shows the top sectors in the fund portfolio. The Real Estate is 48.80% of the total. As will be discussed later, those are primarily large cap and top-quality REIT companies.

RNP Top Sectors and Country Allocation from CEFConnect

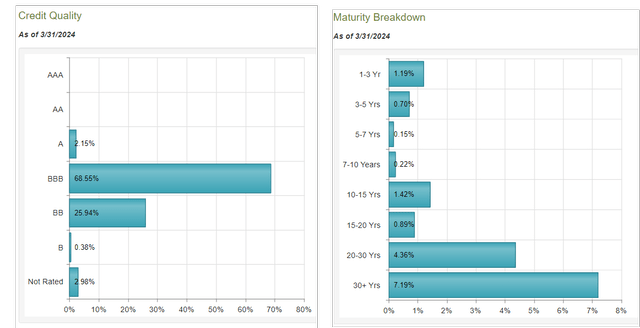

Note that RNP has a substantial portion of the investment in the fixed income assets, including corporate bonds and preferred stocks. The credit is of low quality, mainly for producing high yields, mostly rated BBB (68%) and BB (26%) and with long durations.

RNP Bond Information from CEFConnect

This helps the fund to keep its high yield and maintain a certain level of stability. As a result, the CEF’s volatility level is comparable to ETF VNQ which does not use leverage. RNP has Effective Leverage at 31.49% which is about the average level for CEF of this kind.

Active Management Fund Makes Sense In REIT Market

I have spent a lot of time in the past 12 months analyzing individual REIT stocks. Considering there could be hundreds of properties each REIT invests in, the amount of the time and efforts spent could be tremendous. In the end, I believe that this type of careful due diligence can also be handed off to the industry expert, such as Cohen & Steers and other top names in this space. Adding CEFs and active managed ETFs in the portfolio makes sense in terms of forming a solid foundation as well as a good diversification for my REIT portfolio.

Top-notch management makes the difference. Cohen & Steers is known to be one of the best experts in understanding and managing the real estate assets. Motivated by the fund’s performance, the management tends to pick up the leaders of the growth areas such as cell towers, data centers, industrials, etc. The following is the top 10 REIT holdings (32% of the total). These REITs are big-cap blue-chip stocks in their industries. Many of these are the same stocks as what I have selected based on my own homework.

RNP Top REIT Holdings from CEFConnect

It is important to note that CEF management knows what REITs to avoid. This is actually a CEF edge over the index ETFs, which couldn’t avoid the poor-quality REITs in their portfolios due to the indexing purposes. This edge may often be overlooked and that, in my opinion, is the key for the fund to outperform the benchmark ETFs. The top holdings are typically ended up being very similar for both CEFs and ETFs.

Regarded as one of the best CEFs, RNP has a 5-Star rating from Morningstar, as shown below:

RNP 5-Star Rating from Morningstar

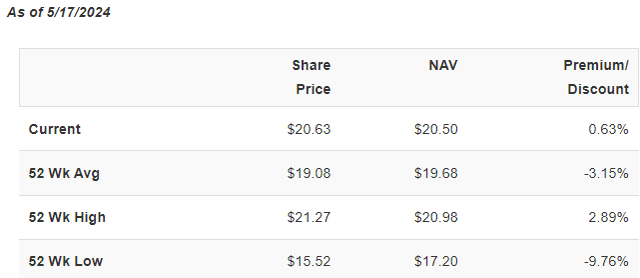

RNP is currently trading at a small premium (0.63%) to NAV. Some investors may hope for some discount, so not to pay more than its current worth.

RNP NAV Information from CEFConnect

While I view this as a justifiable premium for its 5-star status and a very well-managed fund, others may want to see additional catalysts that could propel the upside potential for the fund, especially over the longer haul.

REITs are still in the doghouse, priced at the 5-year ago level with deep NAV discounts

REIT is one sector that is still in the doghouse priced at 5-year ago level. It is the worst performing sector in the market at the moment. I think now is the time to invest in REITs. They are cheap today because they have dropped a lot in the past years due to COVID-19 and the rapid rate hiking from FED. According to S&P Global Market Intelligence data, the REIT sector was at a 19.1% median discount to their consensus on April 30. Valuations are also attractive on a historical basis as they are about 25% cheaper than the historical measure.

From the market perspective, I believe that the “higher for longer” rate regime has already been priced in REIT market. As the time passes along, it becomes increasingly clear that REIT market will bounce back inevitably. With the broader markets keeping making all time highs, it makes little sense to me that the market sentiment is still so bearish-biased towards the REIT sector.

Admittedly, the macro uncertainties such as rate cut, economy, inflation still cast a large cloud in real estate market and keep the REITs on hold, even after these significant rallies in the broad market and the all-time highs achieved by S&P 500 index and Nasdaq 100 index in 2024. However, if the Fed starts to cut the interest rate, not only will it reduce the interest expense burden for RNP, particularly for its high leverage, but the underlying REIT assets in the portfolio will also become more valuable.

In fact, indicated in a recent SA report, “real estate stocks already started to outperform major market averages as rate hikes ruled out, earnings continue to grow”. I think it is quite possible that the REIT market will continue its good run from here.

I am actively constructing my REIT portfolio as part of the income bucket (with a 6% dividend threshold to make the cut) as well as the total value return bucket (with the beaten down sectors). The latter part is based on my expectation of a significant REIT rebound in 2024. RNP plays a good role in my current REIT portfolio.

Risks & Caveats

Higher interest rate will be the main risk for REIT in the short run. The inflation has not been trending down in 2024. Although the FED has ruled out rate hiking recently. It is still possible that the hotter inflation data may force FED to change its rate policy. With higher interest rate, it is also possible for some of the REITs in the ETF’s portfolio to underperform due to the leverage burdens. The fund premium as I discussed earlier could keep the fund from making further price gains.

On the other hand, there are over half of the high-yield holdings that are not REIT equities, they could affect the price gain once a full-blown REIT recovery is on the way. Once that happens, I may look for alternatives with higher weight of REIT holdings.

Conclusion

REIT specialty CEF RNP is considered one of the best CEFs. It offers a very high dividend yield that looks attractive in REIT sector. A moderate rate cut from FED will warrant a highly favorite condition for RNP to outperform its REIT ETF counterparts. RNP’s high leverage could start to work in its favor in the current rate cycle when the rate is peaking off. In addition, it is quite possible for the REIT market to stage a sizeable recovery comeback. REIT investors may find it a very attractive opportunity to buy some shares right now for a great total return in 2024.

Read the full article here

")

")

")

")

")

Place In Emerging Quantum Computing Field")

")